Fourteen months after pandemic panic and economic uncertainty compelled a guarded 2020-2022 outlook for U.S. construction activity, the Portland Cement Association Market Intelligence Group reports that a key indicator of building and nonbuilding project volume actually grew year over year—a trend likely to continue for the near term.

“U.S. cement consumption recorded 2 percent growth during 2020,” says PCA Chief Economist Ed Sullivan, reflecting on internal and U.S. Geological Survey figures behind a spring 2021 forecast update. “It is remarkable because Covid-19 exerted a terrible toll on the economy. Consumers bunkered down; states enacted rigid lockdowns. Real GDP declined to a rate not matched since 1946 as the economy transitioned from war time to peace time. Nearly 9.5 million fewer jobs now exist compared to pre-Covid-19 levels. Many businesses did not survive the threat. And yet through all of this, cement consumption grew.”

While major storms resulted in a weak 2021 start for construction, he adds, it is likely that cement consumption growth will match or exceed 2020’s performance. Record low mortgage rates prompted strong gains in 2020 single family home building. Those rates are expected to remain through 2021, resulting in further strong demand for cement and concrete. Nonresidential construction market declines are likely to continue this year and next, but the drag on overall growth is expected to lessen.

“This recovery is predicated on continued progress in fighting Covid-19. The rapid pace in vaccinations and increased mask usage have resulted in a decline in death rates from over 3,000 daily in January 2021 to less than 825 today,” Sullivan noted upon the spring update’s release last month. “The Institute of Health Metrics and Evaluation [second quarter] forecast suggests a sustained and significant decline in daily Covid-19 deaths to less than 170. Progress associated with Covid-19 is the critical factor in the near-term outlook.”

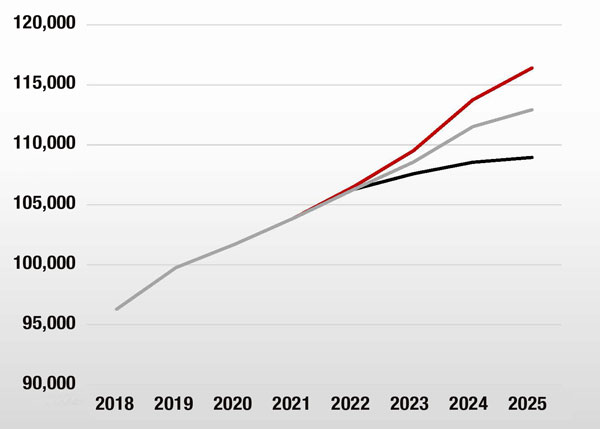

The most significant long-term impact on cement consumption may unfold this year: The White House-proposed $2.2 trillion, eight-year infrastructure program, which expands the traditional definition of infrastructure and contains more than $1.2 trillion in low or no cement intensive projects. If passed as is, the proposal could contribute more than 7 million metric tons annually. In the spring update, PCA Market Intelligence charts that and two other scenarios hinging on Capitol Hill action in which cement consumption through 2025 could climb from about 104 million metric tons this year to 109 million mt (no infrastructure package), 113 million mt (compromise package) or 116 million mt (full White House proposal).

“After committing to spending $5.2 trillion in Covid-19 relief and adding another $2 trillion in operations, the federal U.S. debt could rise $7 trillion dollars in 2020-2021,” Sullivan observes. “This puts the discussion of the proposal into context. The proposal must pay for itself which means higher taxes. While investing in traditional infrastructure such as roads and bridges has bipartisan appeal, tax increases and some programs dubiously labeled as infrastructure has caused concern. This concern threatens the potential passage on the infrastructure initiative.”

POLITICS & POWDER CONSUMPTION

Projected cement shipments (metric tons, 000s) under full $2.2 trillion White House infrastructure proposal, compromise package and no infrastructure package scenarios

WHITE HOUSE • COMPROMISE • NO INFRASTRUCTURE

Source: PCA Spring Cement Outlook, April 2021

ECONOMIST MEASURES PANDEMIC’S FADING EFFECTS ON CONSTRUCTION

An Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics indicates that the construction industry closed out the first quarter adding 110,000 jobs, bringing to 931,000 the number gained since April 2020, or nearly 84 percent of those jobs lost during the early stages of the Covid-19 pandemic. The construction unemployment rate fell to 8.6 percent this March from 9.6 percent the prior month, but it is still 1.7 percentage points higher than a year ago.

“Here comes the tsunami of economic and employment growth across America,” says ABC Chief Economist Anirban Basu. “With more stimulus on the way, the United States may end up growing faster than China this year. Much of the stimulus to come will directly affect construction, particularly the heavy and civil engineering segment. While any infrastructure stimulus should be geared toward projects generating the highest rates of return and open to bids by all competent contractors, the sheer volume of money flowing into the economy is set to create massive forward momentum for the balance of 2021 and likely through 2022. Contractor optimism seems to reflect this building momentum, according to the latest ABC Construction Confidence Index.”

“As always, there are risks,” he adds. “The federal government is borrowing heavily to stimulate the economy. Inflationary pressures are likely to become more apparent during the months ahead, translating into rising interest rates. Already, key construction inputs such as softwood lumber and diesel fuel have experienced sharp price increases over the course of the pandemic. At some point in the future, the U.S. economy could see not only faltering stimulus, a massive national debt and higher costs of capital, but also higher taxes. That does not represent a promising recipe for contractor health. For now, however, it is all systems go.”