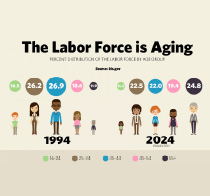

From U.S. Bureau of Labor Statistics Branch Chief Teri Morisi … By 2024, nearly one in four people in the labor force will likely be over the age of 55, a sharp change from 1994, when just under 12 percent of workers were at or above that age threshold. Workers 55 and older will represent the largest share of the 2024 workforce as measured by the other age groups of 16-24, 25-34, 35-44 and 45-54.

There are two factors behind the trend: 1) an aging population of baby boomers, those born from 1946 to 1964, are moving into older age groups; and, 2) older workers’ increasing labor force participation rate. Research shows many older people are remaining in the labor force longer than those from previous generations. According to one study, about 60 percent of older workers with a “career job” retire and move to a “bridge job,” or a short-term and/or part-time position. Another study found that about half of retirees followed nontraditional paths of retirement and did not exit the labor force permanently.

Older workers are choosing to remain in the labor force as they wish to remain healthy and active, have longer life expectancies, and need enough income to live to higher ages. In 2014, Americans at age 65 could expect to live an additional 19.3 years according to the Centers for Disease Control and Prevention, or until about age 84—up about three years since 1980.

Less than 10 percent of private industry employers now offer defined benefit (traditional) retirement plans, while 47 percent offer defined contribution plans, according to data from the Bureau of Labor Statistics’ National Compensation Survey. Defined contribution plans typically include voluntary savings accounts, such as 401(k) plans, in which workers designate deductions from their pay into funds. Earnings from these funds are based on the amount that workers choose to invest and how the funds perform. There is more uncertainty with defined contribution plans versus traditional defined benefit plans, which consist of lifetime periodic payments to the retiree or their spouse.

|

|

| ILLUSTRATION: U.S. Bureau of Labor Statistics |

People may stay in the labor force longer to get a higher Social Security benefit rather than a reduced one if they retire early. Currently, workers can retire at age 62 and receive a reduced benefit, but realize a full benefit if they wait until age 67. The Social Security earnings test was eliminated in 2000 for workers who have reached full retirement age; hence, benefits are not reduced for a worker at the threshold who continues to earn wages. Health coverage is another factor for older persons remaining in the work force, as 65 is the age for Medicare eligibility.